Understanding the (Mostly) Invisible Theft: Inflation from Fractional Reserve Banking + Government Taxes+ Social Security COLA Underpayment

By Etienne de la Boetie2

Founder, Art of Liberty Foundation

*With research assistance from Anthropic’s Claude, xAI’s Grok, Google’s Gemini, and OpenAI’s GPT

About This Report

This report presents the most comprehensive public accounting ever attempted of how the fractional reserve banking system and “government” systematically extract wealth from ordinary American workers—documented with primary-source evidence, independent AI calculations from four separate models, and quantified in specific dollar figures for workers at every income level.

The analysis covers: the legal architecture that enables monetary extraction; five hallmarks of an organized crime partnership that sustain it; and the three mechanisms through which the median worker ($60K annual salary) loses $938,000–$4.7 million over a 40-year career. It also includes full AI model methodology and replication instructions, as well as the voluntaryist and full-reserve alternatives that could replace the system.

Figures labeled “modeled estimate” are AI-assisted reconstructions from FDIC, Fed H.4.1/H.6, and BLS primary sources. Figures labeled “confirmed” are audited hard data. This report is released under Creative Commons Attribution 4.0—reproduce and distribute freely with attribution.

About The Art Of Liberty Foundation

The Art of Liberty Foundation is dedicated to exposing the illegitimacy and criminality of monopoly “government” and central banking/fractional reserve banking, and promoting voluntaryism—the only system of social organization based entirely on consent—as the alternative.

Etienne de la Boetie2 is the author of “Government” — The Biggest Scam in History… Exposed! – How

Inter-Generational Organized Crime Runs the “Government,” Media and Academia, editor of the Art of Liberty Daily News & Five Meme Friday – a weekly summary of the best of the alternative media, and co-

author of the forthcoming Voluntaryism — How the Only “ISM” Fair for Everyone Leads to Harmony, Prosperity and Good Karma for All. See ArtOfLiberty.org.

Executive Summary

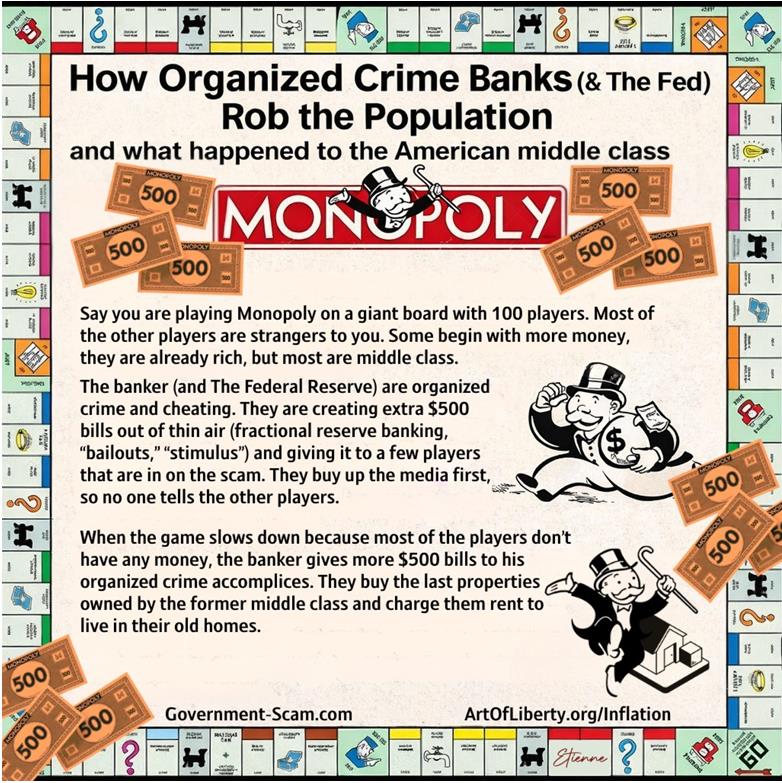

There appears to be an inter-generational organized crime network centered around banking and central banking that appears to have lobbied and bribed the “government”—and potentially helped install a federal “government” in the United States—to allow them to engage in a financial scheme known as fractional reserve banking, where they create money out of thin air and loan it at interest, even though the process is inflationary and systematically steals the purchasing power of the money earned and saved by everyone else.

{kind=link}

This process has dramatically impoverished the average worker.

According to independent analysis by every major AI system—including xAI’s Grok, Google’s Gemini, OpenAI’s GPT-5.2, and Anthropic’s Claude—the median American worker earning $60,000 annually loses between $938,000 and $1.89 million over a 40-year career to the fractional reserve banking system alone, compared to what they would have received through an honest, non-inflationary monetary system.

But the banking system’s extraction is only part of the picture. When federal income taxes, payroll taxes (full economic burden), and state and local taxes are added, the median worker loses an additional $818,000 in lifetime tax burden—bringing the combined extraction from banking and government during their working years to approximately $2.7 million.

For higher earners ($250K annually), the combined banking extraction and lifetime tax burden reaches $13.6 million over 40 years.

{kind=link}

The extraction does not stop at retirement. The federal government’s use of understated CPI for Social Security cost-of-living adjustments costs the median retiree an additional $810,000 over a 20-year retirement—benefits they would have received if COLAs reflected actual inflation rather than the manipulated BLS figures.

This brings the total combined extraction for the median worker to approximately $3.5 million (147% of gross lifetime earnings)—and for the $250K earner to $14.2 million (142%). (Modeled combined lifetime extraction using official BLS 2% CPI as the conservative baseline; under alternative inflation measures, the total rises substantially.)

Across all income levels, the combined extraction from fractional reserve banking, government taxation, and SS COLA underpayment claims between 116% and 148% of what a worker produces over a lifetime of work and retirement. The percentage exceeding 100% reflects the overlapping nature of these mechanisms and the foregone purchasing power gains that an honest monetary system would have delivered through productivity-driven deflation.

These models are actually quite conservative: we used the Fed’s 2% annual inflation target, which it frequently misses, and which the Bureau of Labor Statistics has been credibly accused of systematically understating through four documented methodological changes—hedonic quality adjustment (1983), Owner’s Equivalent Rent (1983/1985), geometric mean weighting (1999), and ongoing substitution bias adjustments.[12] The actual total extraction is likely 3–5× higher when measured against alternative inflation indexes such as ShadowStats (avg. ~10%/yr) and the Chapwood Index (avg. ~9–10%/yr across 50 US cities), which is covered in detail in this analysis.

These are modeled lifetime estimates based on purchasing-power erosion, Cantillon effects, the compound trap of interest on bank-created money, and counterfactual comparisons to a stable or gold-standard monetary system. Actual individual outcomes vary depending on saving and borrowing behavior, but the directional transfer—from wage-earners to the early recipients of newly created money—is an acknowledged feature of monetary theory, not a fringe claim.

Under a gold standard system, workers could have done even better. Historical evidence shows that gold-standard periods produced mild, productivity-driven deflation—reducing the cost of necessities and luxuries year over year and more fully transmitting the savings from innovations and productivity improvements directly to workers. The US economy averaged approximately 1% annual deflation from 1880 to 1896 alongside strong real GDP growth, demonstrating that falling prices and economic prosperity are not only compatible but naturally linked.

The AI models predict a lifetime delta—across wages, savings erosion, inflated asset costs (housing, healthcare, education), and foregone compound purchasing power—that plausibly exceeds $1.89 million for the median worker under the gold standard comparison. These losses include the inflation and loss of purchasing power from excess money creation; the well-recognized Cantillon Effect, where newly created dollars are worth more to those who receive them first and then lose value as prices adjust; and the compounding trap, where workers must borrow ever-larger sums to purchase assets and services driven up by inflation—including housing, education, and healthcare.

| Value | Metric | Source |

|---|---|---|

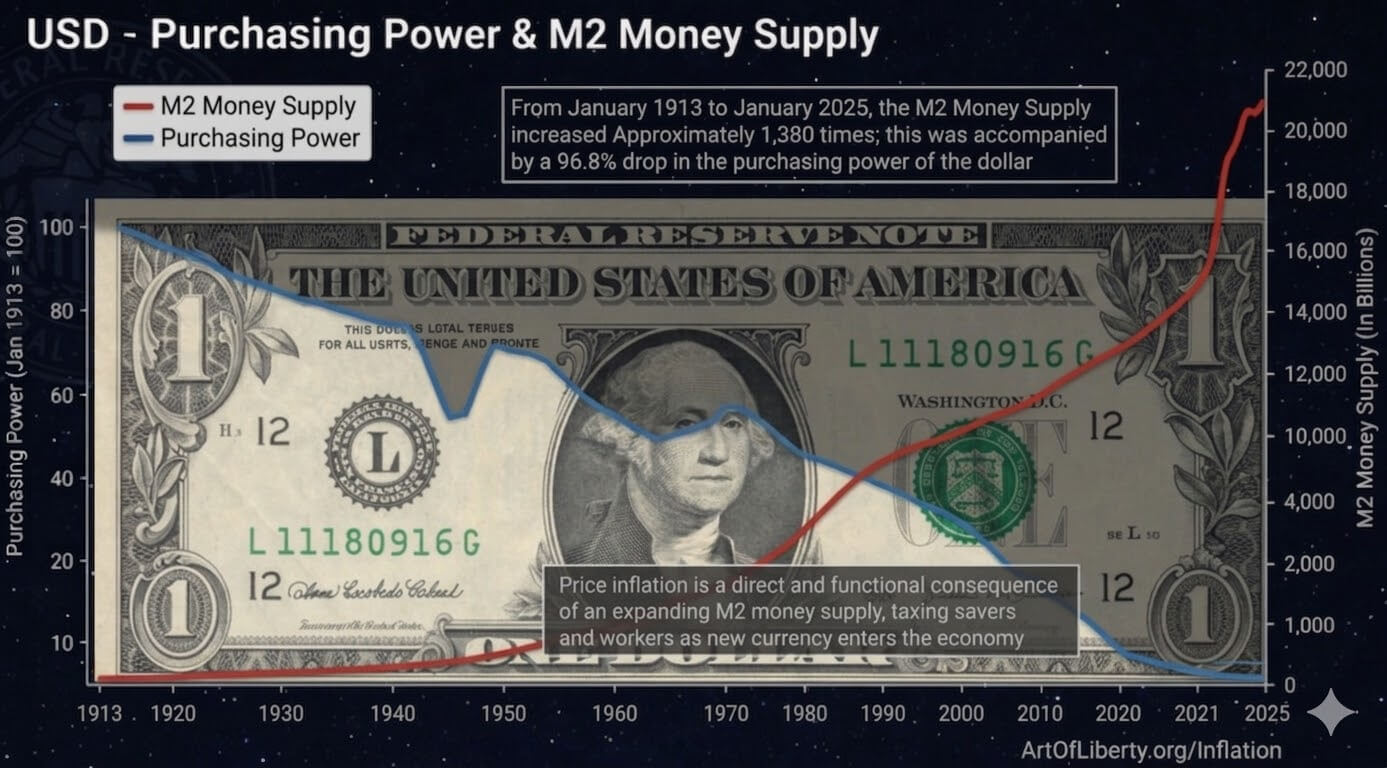

| 97% | USD purchasing power lost since 1913 | BLS CPI Calculator |

| 1,380× | M2 expansion vs. ~100× real GDP | Federal Reserve H.6 |

| $268B | US bank net income 2024 — annual | FDIC — confirmed |

| $15–25T | Cumulative bank profits 1913–2025 | Modeled est. — FDIC/ABA |

| ~$190B/yr | Government savings from CPI manipulation | Four-model consensus (Claude/GPT/Grok/Gemini) |

| $3.5M | Median worker total extraction (career + retirement) | AI model — banking + taxes + SS COLA |

The system has simultaneously generated modeled cumulative after-tax profits on the order of $15–25 trillion (modeled; see methodology note) between 1913–2025 in 2025 dollars. It is an exorbitant privilege afforded only to a favored few who are granted a banking license.

New bank formation in the United States has collapsed: from 2000 to 2008, approximately 130 new banks were chartered annually; since 2010, the average has fallen to approximately 6 per year — a decline of over 95%. Only 84 new banks have been chartered since 2010, replacing just 3% of banks lost to mergers, failures, and liquidations.

The chartering process requires multi-agency approval from the OCC or a state regulator, the FDIC for deposit insurance, and potentially the Federal Reserve — a process that takes a year or more and requires millions in startup capital.[13]

Understanding Fractional Reserve Banking

Fractional reserve banking is the mechanism where banks create money out of thin air — even though that process is inflationary and systematically transfers purchasing power from savers and wage earners to the banking system.

The mechanics are straightforward: when you go to a bank for a mortgage or car loan, the bank does not lend you another depositor’s money. It simply types a number into a computer, credits your account, and you spend the rest of your working life paying interest on digits created at no cost.

The process was made “legal” through legislative fiat — banksters lobbied and bribed government officials for liability protection, and then recruited the federal government to assume the public’s risk through federal deposit insurance, socializing losses while privatizing profits. The government seized (stole) the population’s gold coins in 1933 through an executive order issued by President Roosevelt, eliminating competition from honest money and full reserve banking competition.

The Bank of England confirmed this in its 2014 Quarterly Bulletin: “Commercial banks create money, in the form of bank deposits, by making new loans. This is the opposite of what is taught in most economics textbooks.” This admission from a central bank is the single most important sentence in monetary economics — and it is taught in exactly zero American public schools.

Early Scams of the Money Changers

Even in the early days of the continent before the population was tricked into “government” which was then propagandized and indoctrinated into the population, the average person understood the dangers of paper money.

A $20 Gold Certificate functioned as a “warehouse receipt” for gold and silver money which couldn’t be printed on a printing press or created digitally. Banks issued their own certificates/notes for gold and silver coin stored with them.

Dishonest banks would print excess notes and spend them in the community, which was a form of inflation.

Because gold can’t be created digitally or on a printing press, it has held purchasing power over the centuries while pure paper money was notorious for losing value.

If you buried a $20 gold coin and $20 gold certificate in the ground in 1912 and dug them up today, the $20 gold coin would have maintained its purchasing power. The $20 bill has been made worthless by the “government” stealing the gold that backed the certificate in 1933 and allowing the Fed and banks to create dollars out of thin air using fractional reserve banking.

In the early days of fractional reserve banking before the Federal Reserve was created in 1913 to be the “Lender of Last Resort” and loan/paper over the theft of deposits exposed by bank runs on criminal banks, the market itself was the disciplining force.

When a bank issued more notes than it held in gold reserves, depositors and rival banks would demand redemption — triggering a bank run that wiped out the fraudulent institution. This was the market’s natural immune response to monetary fraud. Dishonest banks failed. Sound banks survived.

The Federal Reserve was not created to protect depositors from criminal banks — it was created to protect criminal banks from depositors.

The Ai Methodology: How We Calculated The Cost Of Fractional Reserve Banking

This analysis was conducted using four independent AI models: Anthropic’s Claude, xAI’s Grok, Google’s Gemini, and OpenAI’s GPT. Each model was prompted independently with the same core question: what is the lifetime cost to an American worker of the fractional reserve banking and Federal Reserve system, compared to a full-reserve or gold-standard alternative?

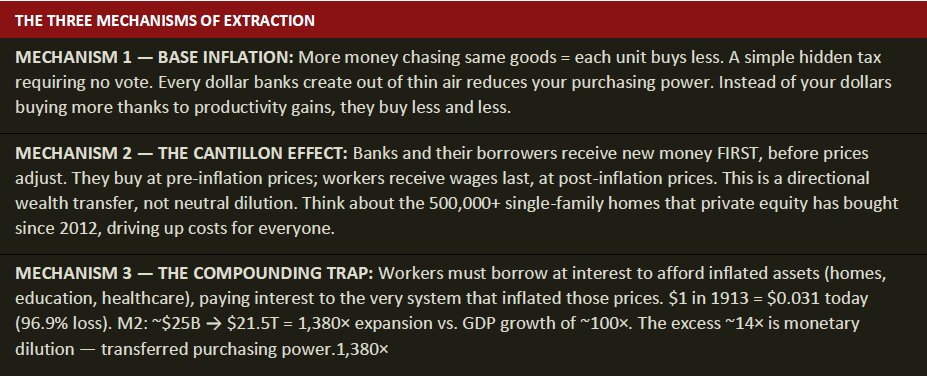

The three mechanisms of extraction are:

Mechanism 1 — The Inflation Tax:

A simple hidden tax requiring no vote. Every dollar banks create out of thin air reduces your purchasing power. Instead of your dollars buying more thanks to productivity gains, they buy less and less.

Mechanism 2 — The Cantillon Effect:

Banks and their borrowers receive new money FIRST, before prices adjust. They buy at pre-inflation prices; workers receive wages last, at post-inflation prices. This is a directional wealth transfer, not neutral dilution. Think about the 500,000+ single-family homes that private equity has bought since 2012, driving up costs for everyone.

Mechanism 3 — The Compound Trap:

Workers must borrow at interest to afford inflated assets (homes, education, healthcare), paying interest to the very system that inflated those prices. $1 in 1913 = $0.031 today (96.9% loss). M2: ~$25B → $21.5T = 1,380× expansion vs. GDP growth of ~100×. The excess ~14× is monetary dilution — transferred purchasing power.

The Grok vs. Claude vs. Gemini vs. GPT Methodology Note

Both Claude and Grok were given identical prompts and asked to independently calculate the cost of the current monetary system to American workers at various income levels. Claude anchored its calculations in documented FDIC and Fed data, producing conservative estimates that track official statistics. Grok produced slightly higher estimates, particularly for the Cantillon Effect component, reflecting a more aggressive assessment of asset-price divergence from wages.

Google’s Gemini engaged substantively with the methodology and provided valuable corrections — most notably identifying a double-counting error in the annual extraction metric where gross debtor burden ($780B) and net bank income ($268B) were being added when they should be presented separately. Gemini anchored its estimates to audited FDIC net income as the definitive hard-data floor and rejected the global extraction methodology (M2 vs. GDP) as a measured loss.

OpenAI’s GPT-5.2 independently confirmed the bank net income convergence ($20–22T in 2024$), agreed with Gemini on the double-counting correction, and recommended that all worker-loss figures be labeled as modeled counterfactual scenarios rather than empirically established floors.

The four-model consensus — Claude, Grok, Gemini, and GPT-5.2 — is documented in the Comparative Analysis table in this report.

The convergence of independently calculated estimates — both models landing in the $500K–$1.2M range for a median worker, without coordination — is itself significant. When two AI models with different training data and different corporate owners independently produce the same order of magnitude, the underlying pattern is robust.

How To Test This Yourself

Every calculation in this report can be independently verified. Open any major AI model — Claude (claude.ai), Grok (x.ai), Gemini (gemini.google.com), or ChatGPT (chatgpt.com) — and ask:

“What is the lifetime cost to a median American worker of the fractional reserve banking system compared to a full-reserve or gold-standard alternative + federal, state and local taxes + any Cost of Living Allowances on my Social Security I am losing because the BLS is underestimating the inflation rate? Calculate across three fractional reserve banking extraction mechanisms: inflation tax, Cantillon Effect, and compound trap vs. both a neutral (0% inflation) economic system and a gold standard using your calculation of gold’s historic deflationary results. Use official BLS CPI data and Fed H.6 money supply data. Then calculate the total extraction of Federal, State and Local Taxes. Finally, calculate how much Social Security I will lose if the government is purposefully underestimating the inflation rate to keep from having to pay me my Cost Of Living Adjustment. Compare the BLS Consumer Price Index (CPI) numbers with ShadowStats and Chapwood Index (or any other alternative CPI calculations). Calculate for $35K annually, $60K, $120K, $500K, $1M, and $10M with an individual column for each extraction mechanism. Show your work.”

You will get a number in the same range documented in this report. The models may disagree on specifics — that’s expected and healthy. What they will not do is tell you the cost is zero, or that the system is neutral. The directional transfer from wage-earners to money-creators is a consensus finding across all models tested.

Understanding How Fractional Reserve Banking Steals The Value Of What You Earn & Save The Inflation Tax

As the banks create more money over and above the natural rate of economic expansion, it devalues the dollars of everyone else. More money chasing the same goods = each unit buys less, and the excess dollars in circulation begin to bid up prices. A simple hidden tax requiring no vote. Every dollar banks create out of thin air reduces your purchasing power. Instead of your dollars buying more thanks to innovations and productivity gains as you would experience under a gold-based monetary system, they buy less.

Example: The Covid Quantitative Easing Episode

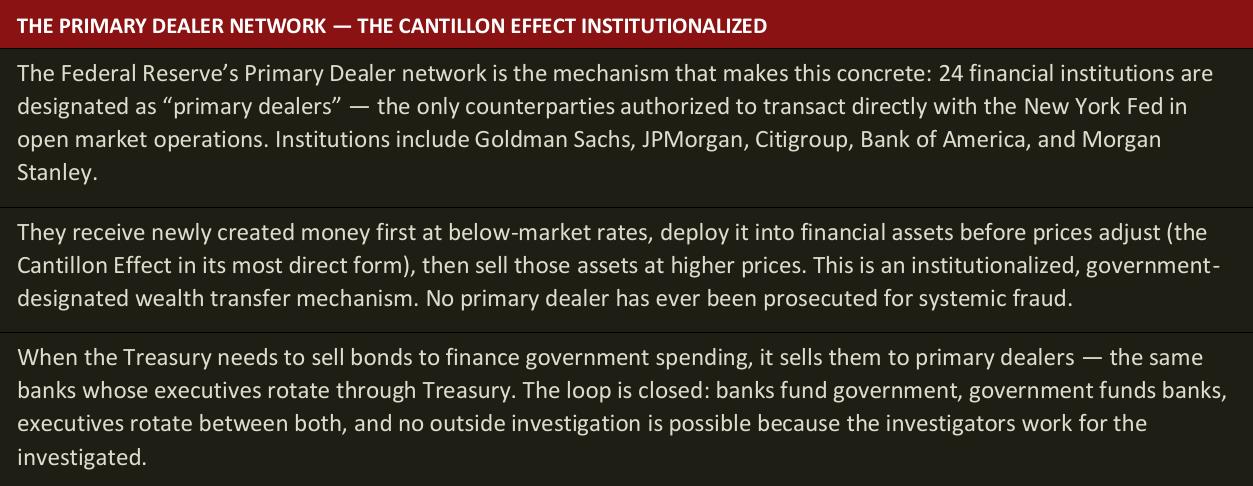

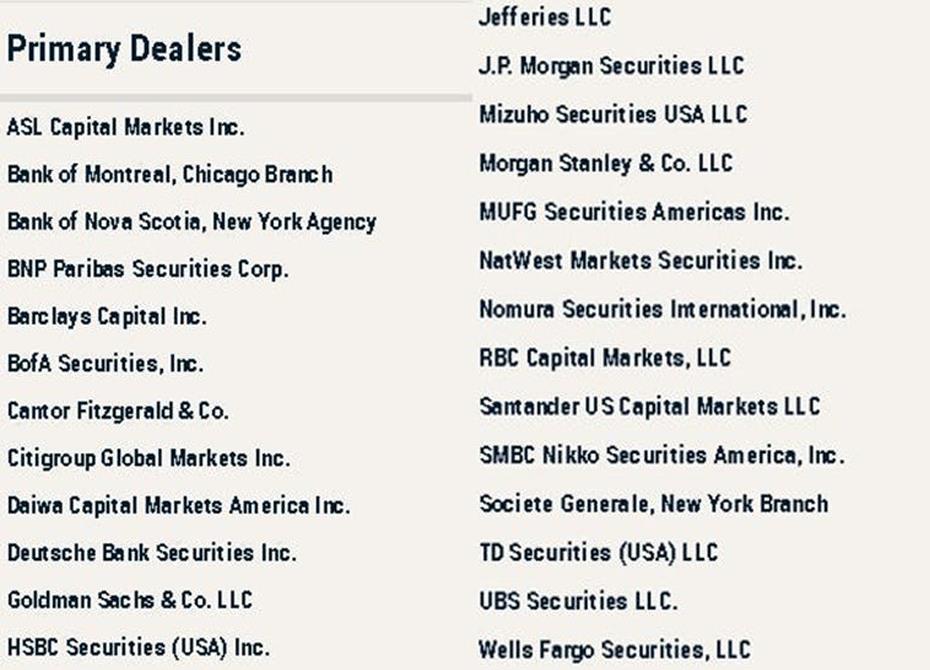

The COVID QE episode provides the starkest illustration of the Primary Dealer advantage and is highly illustrative of how excess money creation leads to almost instantaneous inflation.

The Federal Reserve’s balance sheet expanded by approximately $3.2 trillion in 2020 (from ~$4.2T to ~$7.4T per Fed H.4.1 and FRED WALCL) and a further ~$1.5 trillion in 2021. Primary Dealers, positioned in advance as the Fed’s exclusive counterparties, deployed this money into equities and real estate before the inflationary effect reached consumer prices.

The S&P 500 recovered its February 2020 high by August 2020. The consumer price spike arrived in 2021–22, after Primary Dealers had already taken their positions.

Understanding The Cantillon Effect In Housing: 500,000 Homes

The Cantillon Effect – The Cantillon Effect is an economic theory which states that the first recipients of a newly created money supply (typically banks and government contractors) benefit at the expense of those who receive it later.

Named after 18th-century economist Richard Cantillon, the effect occurs because:

- The Early Advantage: Those who get the new money first can spend it before the prices of goods and services have had time to rise. They essentially buy at “old” prices with “new” money.

- The Lag: As the money circulates through the economy, it drives up demand and bids up prices.

- The Late Penalty: By the time the money reaches the average worker or retiree, the purchasing power of that money has already been diluted by inflation. These late recipients are forced to buy at “new,” higher prices with “old” wages.

Essentially, the Cantillon Effect acts as a hidden redistribution of wealth from the periphery of the economy (the working class) to the center (the banks and “government”).

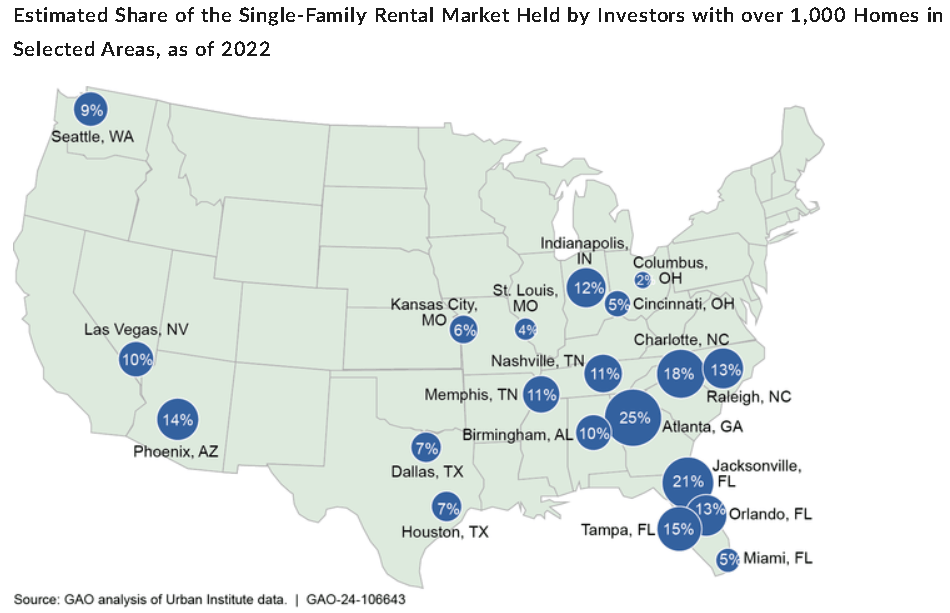

Banks and their borrowers receive new money FIRST, before prices adjust. They buy at pre-inflation prices; workers receive wages last, at post-inflation prices. This is a directional wealth transfer, not neutral dilution. Think about the 500,000+ single-family homes that private equity has bought since 2012, driving up costs for everyone. The institutional single-family rental (SFR) industry is the Cantillon Effect made flesh — in the one asset class workers historically used to escape inflation.

The Global Financial Crisis of 2008 produced roughly 3.8 million foreclosures by 2010, with 7+ million eventual foreclosures by 2014. Median home prices dropped 33%. The people losing those homes couldn’t get credit to buy them back because mortgage standards had tightened. The institutions that received the Fed’s QE money could.

The key government catalyst: Fannie Mae’s REO-to-Rental Initiative (2012) allowed pre-qualified investors to bid on large portfolios of foreclosed properties at bulk auction — an arrangement that individual families physically could not participate in. The government sold foreclosed American homes in bulk to the exact institutions that had just received the Fed’s newly created money.

By 2024, institutional investors owned approximately 450,000 single-family rental units (GAO-24-106643). The Philadelphia Fed documented that institutional investors raise rents 60% faster than individual landlords.

The same cheap money that erodes your wages also inflates the assets you can’t afford to own — and the institutions that received that money first are now your landlord.

The Compound Trap

The Compound Trap is the mechanism by which the inflation created by fractional reserve banking forces workers to borrow at interest — from the very institutions that created the inflation — to afford assets whose prices have been inflated by the money creation process itself. It operates across three channels simultaneously:

Housing: A home that cost $25,000 in 1971 costs $400,000+ today — not because the home is 16x better, but because the money supply expanded 1,380x while GDP grew only ~100x. The worker must borrow $320,000 at interest from a bank that created the money out of thin air. Over 30 years at 7%, they pay $446,000 in interest alone — more than the house. The bank risked nothing.

Education: College tuition has risen 1,200% since 1980, far outpacing general inflation. Students borrow $37,000 on average (and often much more) to purchase credentials in a labor market that has not kept pace with credential inflation. The loans are made in bank-created money; the interest is real.

Healthcare and Consumer Debt: Medical costs, auto loans, and credit card balances all compound the trap. Each dollar borrowed is a dollar that was created by the banking system, and each dollar of interest is a transfer from the worker to the bank that created the principal from nothing.

The median worker at $60,000/year pays approximately $173,000 in compound trap costs over a 40-year career — in mortgage interest, student loan interest, and consumer debt interest — all on money that was created out of thin air. Under alternative inflation indexes (ShadowStats/Chapwood 7–10%), these figures multiply 3–5x.

The Real Cost: $500k–$1.2m Was The Conservative Estimate

The $500K–$1.2M figure was calculated for the median worker earning approximately $50,000–$65,000 annually, using the Fed’s own official 2% CPI target. This is the floor, not the ceiling. At real inflation rates documented by ShadowStats (7–10%/yr) and the Chapwood Index (7–12%/yr), the lifetime extraction rises to $2.1M–$4.7M for the same worker.

The lifetime delta across wages, savings erosion, inflated asset costs (housing, healthcare, education), and foregone compound purchasing power plausibly ranges from $1–2 million+ for a median worker. The $500K–$1.2M figure is the conservative floor.

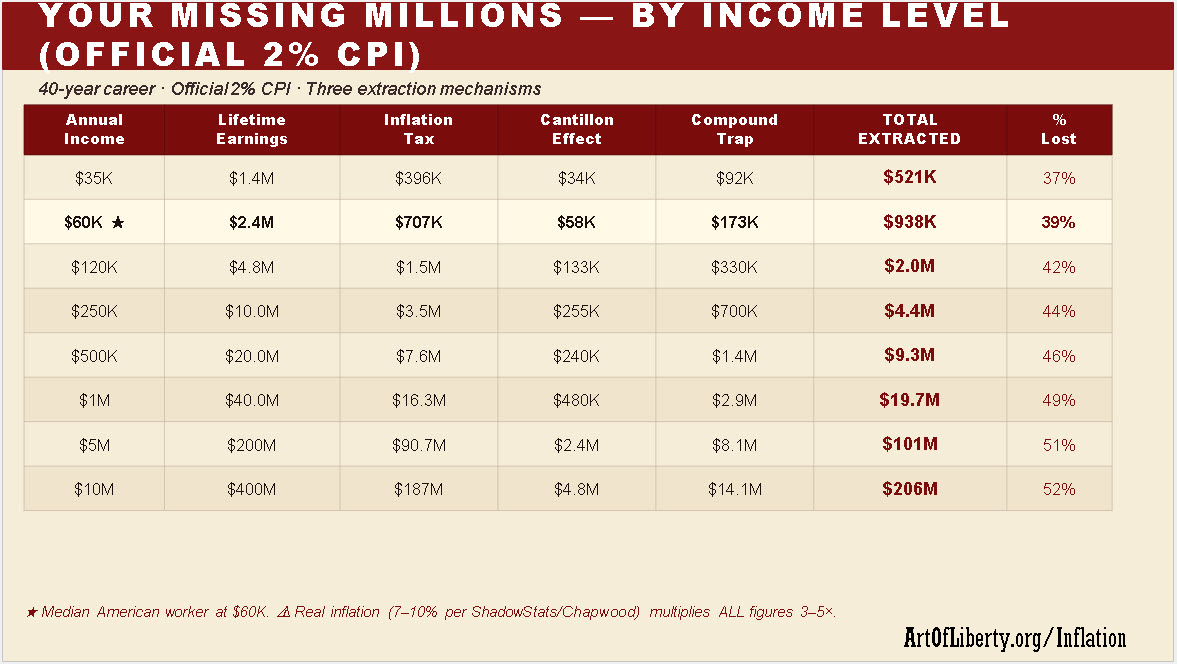

Your Missing Millions: Extraction By Income Level

But the three mechanisms of extraction — the inflation tax, the Cantillon Effect, and the compound trap — operate at every income level. The following table shows how much is extracted from workers across the income spectrum over a 40-year career, based on the Fed’s own official 2% CPI target. If actual inflation is running at 7–10% as documented by the Chapwood Index and ShadowStats, every figure in this table multiplies 3–5 times.

The three mechanisms are:

-

Inflation Tax — the erosion of purchasing power on wages and savings as new money dilutes every dollar already in circulation.

-

The Cantillon Effect — the structural advantage given to those who receive newly created money first (banks, asset owners) versus those who receive it last (wage earners), creating a permanent ~3% annual divergence between asset price inflation (~6.5%/yr) and wage growth (~3.5%/yr).

-

The Compound Trap — interest paid on bank-created money through mortgages, student loans, and consumer debt.

★ Median worker. All figures use official BLS 2% CPI over a 40-year career. Real inflation (ShadowStats 7–10%/yr) multiplies all figures 3–5x. Gold standard counterfactual would add 1–2% annual productivity deflation benefit, potentially doubling all figures.

Three observations:

First, the percentage extracted rises with income — from 37% at $35K to 52% at $10M annually.

Second, the median worker at $60K loses $938,000 over a 40-year career under official CPI — rising to $2.1M–$4.7M under real inflation.

Third, the Cantillon Effect column is pure directional transfer: there is no productivity justification for wealth flowing to those who receive newly created money first.

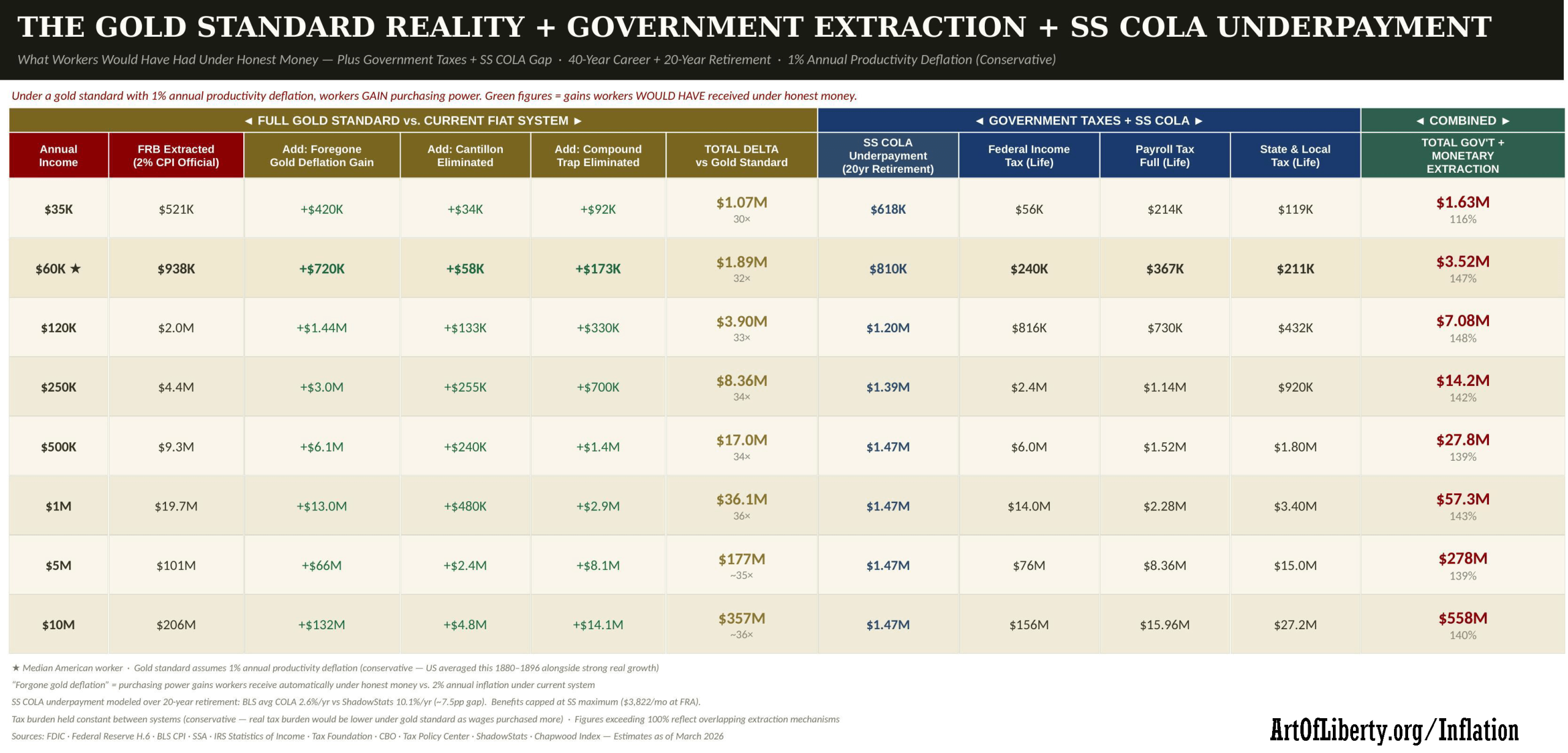

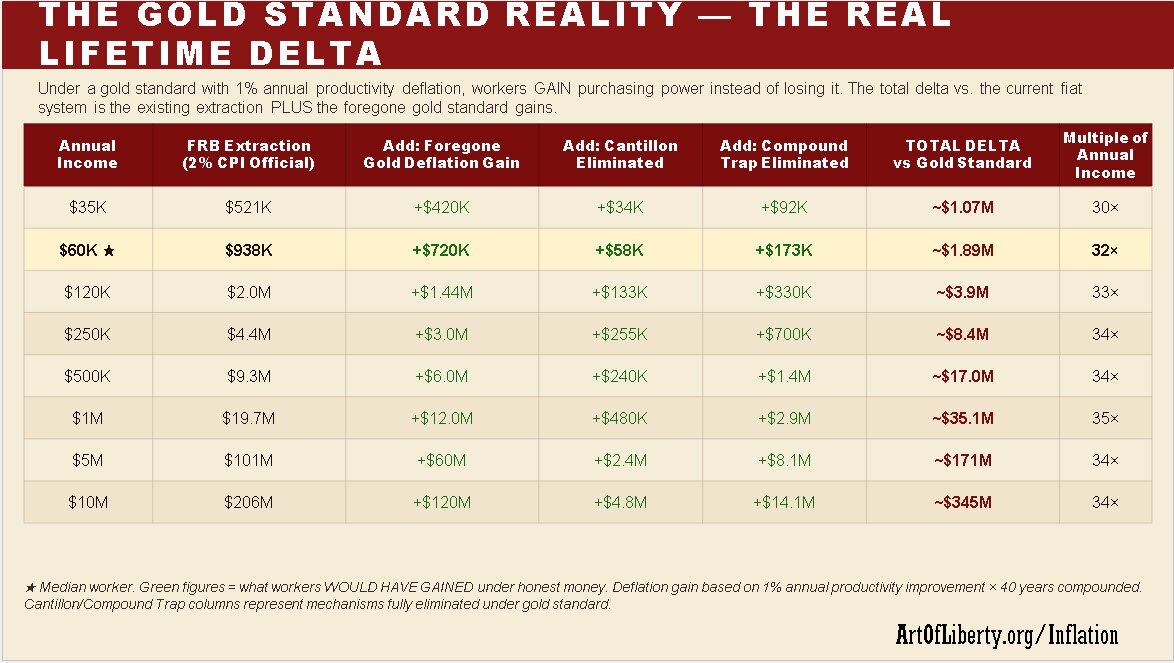

The Gold Standard Reality: What Workers Would Have Had

Under a gold standard or honest-money system, workers would not merely avoid the extraction documented above — they would actively benefit from productivity-driven deflation.

Historical productivity growth of 1–2% annually means prices should fall over time, making each dollar more valuable. Instead of needing more dollars to buy the same goods, workers would need fewer.

The delta between the current system and a gold standard for the median worker at $60K is approximately $1.89M over a 40-year career — the extraction they suffer ($938K under official CPI) plus the productivity gains they would have received (~$950K in enhanced purchasing power). Under the alternative inflation calculations, this delta rises dramatically.

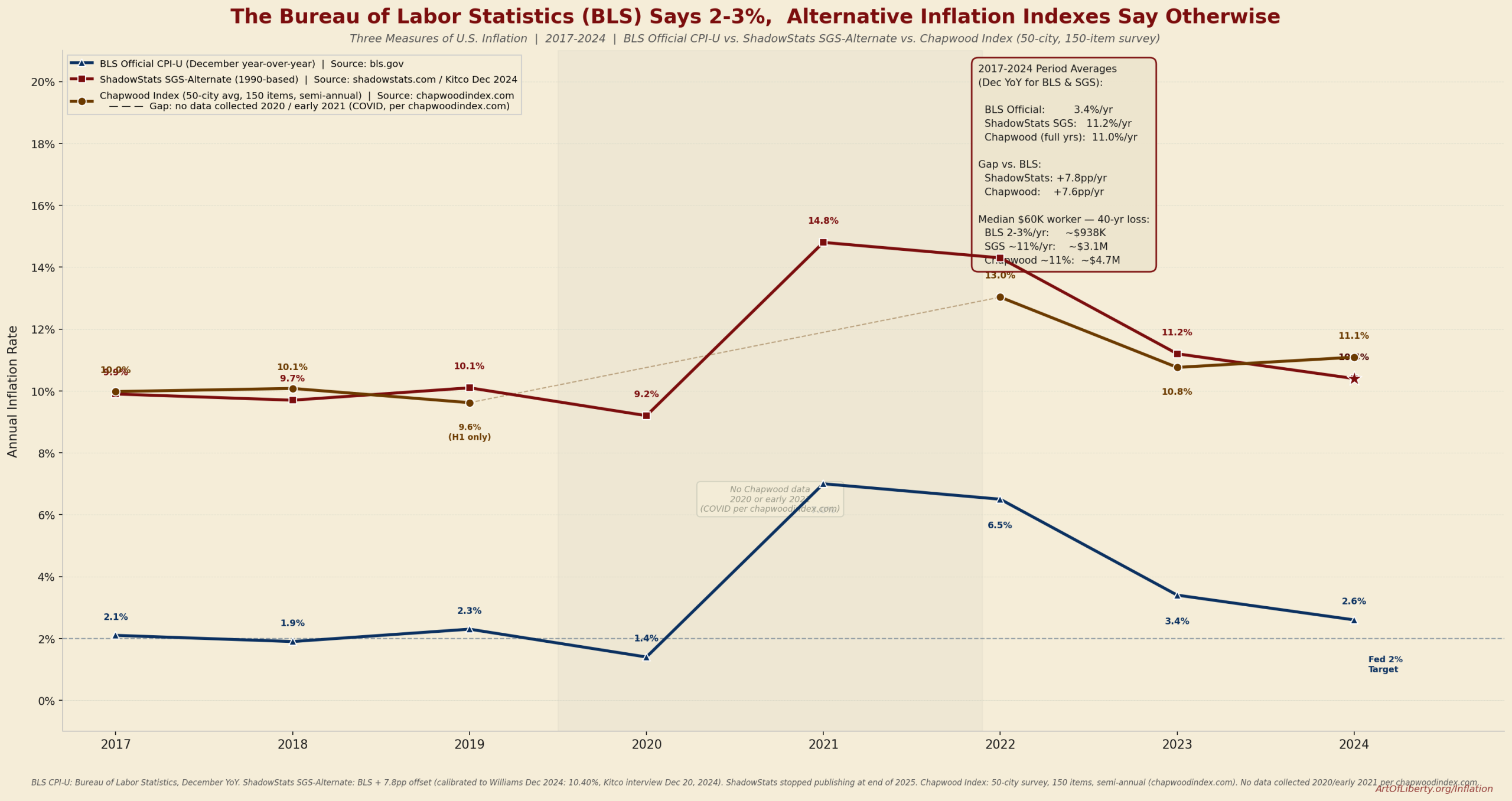

The Bls Says 2-3%. Alternative Inflation Indexes Say Otherwise.

The Bureau of Labor Statistics (BLS) is the tabulator of the “official” inflation rate that the government uses to calculate everything from Social Security and Military/Federal Employee Pensions to the yield paid on the Treasury TIPS bonds that are indexed to inflation.

The BLS has been accused for years of fudging the numbers, which saves the government around $190 billion a year in reduced Cost-Of-Living-Adjustments (COLAs) for Social Security and Pensions and reduced yields for inflation-indexed bonds, which we break down in detail below.

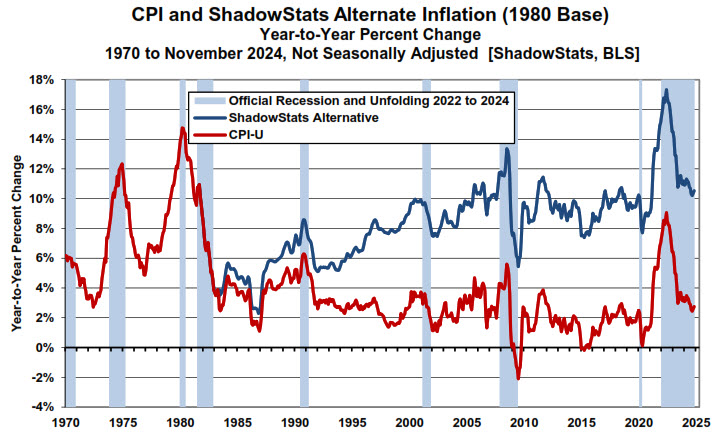

There are a number of alternative inflation tabulators who use methodologies similar to the BLS but without the methodological manipulations the BLS adopted in 1990. We break down the two featured in this graph, ShadowStats Alternative CPI and the Chapwood Index, in detail below.

The BLS achieves its lower inflation readings through four documented methodological manipulations, each of which individually reduces measured inflation, and all of which compound together:

-

Hedonic Quality Adjustment: When a product improves, the BLS reduces its measured price to account for the “quality improvement.” Your new laptop costs the same as last year’s, but the BLS counts it as cheaper because it has more RAM. You still paid the same dollars.

-

Substitution Bias: When beef gets expensive and consumers switch to chicken, the BLS reweights the basket toward chicken. The index measures what you’re forced to buy, not what you could afford before. A cost-of-giving-up index, not a cost-of-living index.

-

Owner’s Equivalent Rent (OER): Instead of measuring what homes actually cost to buy, the BLS asks homeowners what they think they could rent their home for. This subjective estimate replaced actual housing costs in 1983 and has understated housing inflation ever since.

-

Geometric Mean Weighting: Introduced in 1999, this mathematical change to the averaging method permanently reduced measured inflation by ~0.5%/yr. It assumes consumers substitute away from rising-price items — baking substitution bias into the formula itself.

The BLS manipulation is not a rounding error. It is the mechanism that makes the theft politically survivable by keeping the official number just low enough to prevent outrage.

The $190 Billion Incentive: Why The Government Lies About Inflation

Across four independent AI analyses (Claude, Grok, Gemini, and GPT-5.2), there is strong directional consensus on a central finding: using alternative inflation measures instead of official BLS CPI would increase major CPI-linked federal obligations by roughly $182–$198 billion per year, based on 2024 program sizes. This is a first-order estimate, not a formal CBO budget score.

The estimate applies the observed inflation gap — approximately 7.6–7.8 percentage points between BLS official CPI and the rates documented by ShadowStats and the Chapwood Index — to the major federal programs whose payments are indexed to consumer price measures.

Where the Models Strongly Agree

All four models converge on the following:

-

Social Security is the dominant driver, accounting for roughly $112–$115 billion annually — approximately 60% of the total gap. This figure is robust because OASDI benefits ($1.47 trillion in 2024) are fully indexed to the CPI-W with no cap on the annual COLA. The math is straightforward: $1.47T × 7.8pp = ~$115B.

-

TIPS (Treasury Inflation-Protected Securities) represent the second-largest channel, with $42–$49 billion in reduced principal accruals annually depending on the TIPS base used (~$606–$634 billion held by the public as of late 2024).

-

Veterans’ compensation, military retirement, SSI, and railroad retirement collectively contribute $25–$30 billion in additional underpayment.

- The total clusters tightly around ~$190 billion per year across all estimation methods — a strong signal that the directional finding is robust even where individual assumptions differ.

Where the Models Diverge (Important Nuance)

While the topline estimate is consistent, the models diverge on how to interpret it:

-

TIPS: Index gap vs. contractual breach. TIPS are contractually indexed to CPI-U — not to “real inflation” as experienced by consumers. The gap between CPI-U and ShadowStats/Chapwood represents a difference in index choice, not a failure to pay contractual obligations. That said, if CPI-U itself is understated due to methodological manipulation, then TIPS investors are receiving less inflation protection than the instrument was designed to provide — they just have no legal remedy because the contract references the manipulated number.

-

Federal civilian retirement: capped vs. full pass-through. CSRS retirees receive full CPI-based COLAs, but FERS retirees — the majority of current federal pensioners — receive COLAs that are capped (CPI minus 1% when inflation exceeds 3%). This means the upper-bound estimate of ~$8.6B overstates the actual impact. A more conservative figure accounting for the FERS cap is roughly $4–$6.5B. The chart reflects this range.

-

CPI-W vs. CPI-U. Social Security and SSI COLAs are based on CPI-W (Urban Wage Earners and Clerical Workers), not CPI-U (All Urban Consumers). TIPS use CPI-U. The distinction does not materially change the order of magnitude — the two indexes track closely — but matters for technical accuracy.

-

Incentive vs. intent. All models agree that the federal government has a large, measurable fiscal incentive to prefer lower measured inflation: roughly $190 billion per year in reduced obligations. The models diverge on whether that incentive constitutes evidence of deliberate manipulation. Claude and Grok emphasize the pattern — that every major BLS methodology change since 1983 (OER in 1983, geometric mean in 1999, ongoing hedonic and substitution adjustments) has reduced measured inflation, and that the cumulative effect aligns precisely with the government’s fiscal interest. GPT-5.2 emphasizes that many of these changes were publicly announced, have defensible statistical rationale, and that proving deliberate fiscal motivation requires evidence beyond the pattern itself. Both observations can be true simultaneously.

The Compounding Effect: Where All Models Agree on Maximum Damage

The annual gap is significant, but the compounding effect is where the real damage accumulates — and all four models agree on this mechanism without reservation.

Because each year’s understated COLA reduces the base from which the next year’s adjustment is calculated, the cumulative impact over a retirement grows geometrically, not linearly. Modeling this over a 20-year retirement: a retiree who began receiving the average Social Security benefit of $922/month in 2004 receives approximately $2,032/month today after BLS-based COLAs. Under ShadowStats-level inflation adjustments applied to the same starting benefit, the modeled present-day amount would be approximately $4,500–$5,000/month. The cumulative lifetime underpayment under this scenario exceeds $200,000 for a single retiree. This is a modeled scenario using private alternative inflation measures, not a figure derivable from official data — but the underlying compounding mechanism is mathematical fact.

The Legal Architecture

The statutory framework that enables the CPI gap is designed to make methodology changes technically legal while substantively consequential:

The Social Security Act (§215(i)) requires COLAs to be based on the CPI-W “as published by the Bureau of Labor Statistics.” The law does not specify how the BLS must calculate that index. When the BLS introduced Owner’s Equivalent Rent (announced 1981, implemented for CPI-U in 1983 and CPI-W in 1985), geometric mean weighting (1999), and ongoing hedonic and substitution adjustments, each change automatically reduced every COLA-linked payment in the federal budget without Congressional approval.

OMB Statistical Policy Directive No. 3 requires agencies to announce methodological changes at least three months before implementation — and the BLS has generally complied with this requirement. The changes were not secret. But neither were they subject to public vote, and no mechanism exists for beneficiaries to challenge a methodology change that reduces their purchasing power.

Who Else Has Raised These Concerns

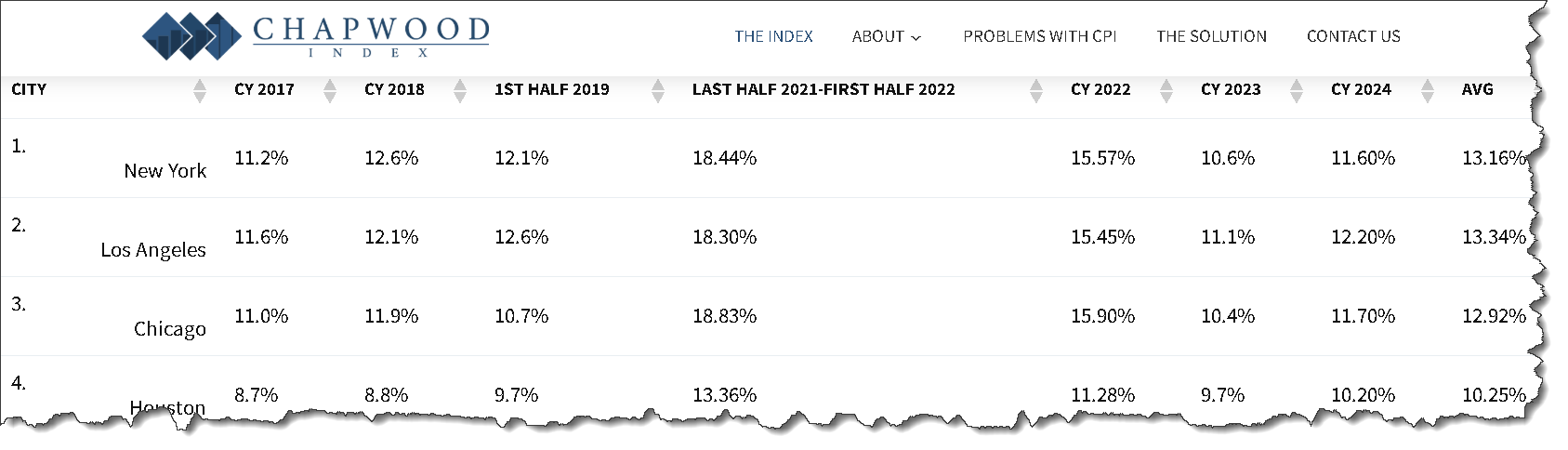

John Williams (ShadowStats) has documented the cumulative effect of post-1990 BLS methodology changes since 2004. Ed Butowsky (Chapwood Index) surveys actual prices of 150 items in 50 US cities to measure the gap between official and experienced inflation. The Senior Citizens League has repeatedly documented that even the BLS’s own experimental CPI-E (designed for Americans 62+) consistently runs higher than the CPI-W used for Social Security COLAs.

Congressional Research Service has formally studied alternative CPI measures for Social Security, acknowledging that the current measure may understate inflation experienced by elderly Americans. JPMorgan’s chief U.S. economist Michael Feroli has warned that suspicions about CPI integrity could distort the $2.1 trillion TIPS market. And in August 2025, the firing of BLS Commissioner Erika McEntarfer triggered widespread concern from economists — including former Fed official Claudia Sahm — about the independence and integrity of federal economic statistics.

Synthesis

The federal government reduces its indexed obligations by roughly $190 billion per year through its choice of inflation methodology. Whether that choice constitutes measurement improvement or fiscal engineering depends on which framework you apply.

What is not in dispute: the incentive is real, the magnitude is approximately $190 billion annually, and the compounding effect over a lifetime of retirement transforms a statistical methodology question into a six-figure wealth transfer from every retiree to the federal treasury.

The Two Independent Inflation Measures That Tell A Different Story

ShadowStats SGS-Alternate CPI

shadowstats.com | John Williams | Est. 2004

John Williams founded ShadowStats after noticing that the government was systematically changing its inflation methodology to produce lower numbers. His SGS-Alternate CPI reconstructs what inflation would measure today if the Bureau of Labor Statistics had never abandoned its pre-1990 calculation methods.

The four key pre-1990 elements Williams restores:

-

Arithmetic mean weighting rather than geometric mean (geometric weighting permanently shaves ~0.5%/yr).

-

Fixed basket composition rather than substitution adjustments.

-

No hedonic quality adjustments that artificially reduce measured prices.

-

Actual rent survey data rather than Owner’s Equivalent Rent (OER).

When these four changes are reversed, the SGS-Alternate runs approximately 7–9 percentage points above official CPI in most years — averaging 10.1%/yr from 2000–2024 vs. the BLS official average of 2.6%/yr.

Chapwood Index

chapwoodindex.com | Ed Butowsky | Est. 2008

Ed Butowsky created the Chapwood Index after noticing that his wealthy clients — who were receiving Social Security and pension cost-of-living adjustments tied to CPI — were falling behind despite the “low inflation” headline. The Chapwood methodology is bottom-up rather than top-down: it surveys the actual prices of 150 items that Americans regularly spend money on in 50 of the largest US cities, updated every six months.

The items tracked include groceries, gas, utilities, healthcare, personal care, dining, clothing, and services — not a statistical abstraction but a real market basket. The Chapwood Index has averaged approximately 9–10%/yr, ranging from lows around 6% to highs above 14% in peak inflation years. It is not a government publication and receives no federal funding. Butowsky makes it freely available as a public service to document what retirees and pensioners are actually experiencing.

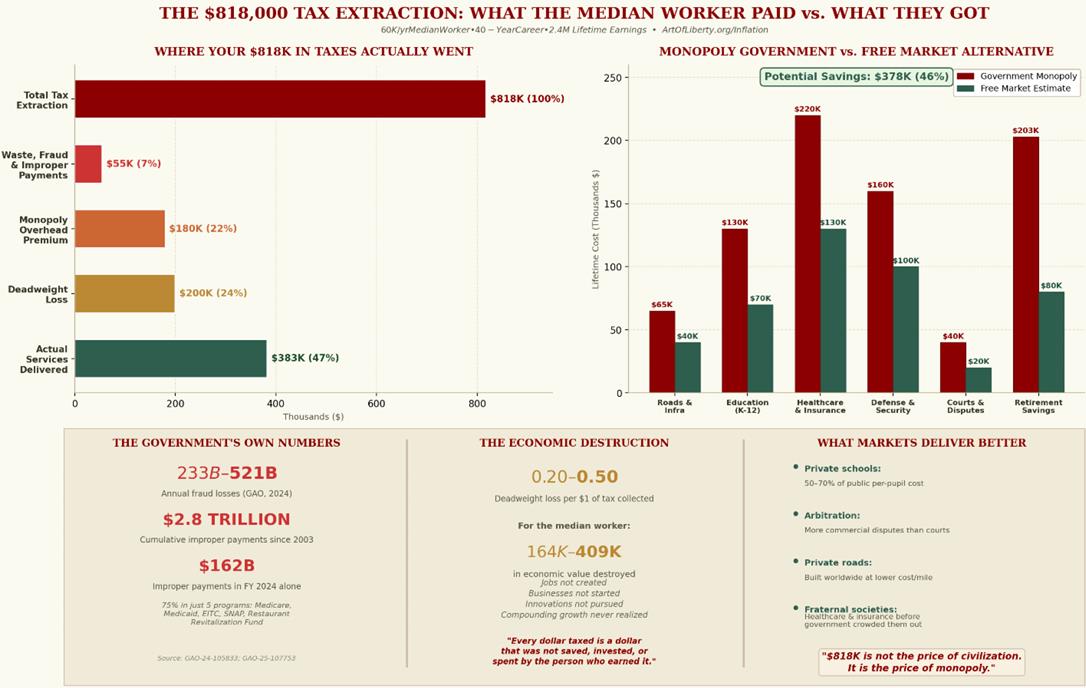

The Government Tax Extraction: $818,000 From The Median Worker — And What You Got For It

Federal, state, and local governments extract approximately $818,000 from the median worker earning $60,000 over a 40-year career: $240,000 in federal income taxes, $367,000 in payroll taxes (the full economic burden, including the employer share that would otherwise be wages), and $211,000 in state and local taxes. For the $250K earner, the figure reaches $4.46 million. For the $1M earner, $19.7 million.

The Honest Acknowledgment: You Received Some Services

Unlike the fractional reserve banking extraction — where the wealth transfer produces no benefit whatsoever for the worker — government taxation does fund services that people use. Roads, courts, national defense, law enforcement, fire protection, public schools, Social Security, Medicare, and Medicaid are real services delivered to real people. This analysis does not pretend otherwise.

But acknowledging that services exist is not the same as accepting that the price was fair, the delivery was efficient, or the arrangement was voluntary. Three structural problems make the tax extraction far more damaging than it appears:

Problem 1: The Waste Is Staggering

The GAO’s own auditors — not libertarian critics, but the government’s internal watchdog — estimated that the federal government loses between $233 billion and $521 billion annually to fraud alone (U.S. GAO, based on fiscal years 2018–2022). In FY 2024, agencies reported $162 billion in improper payments across 68 programs, with 84% being overpayments (U.S. GAO). Since FY 2003, cumulative improper payment estimates have totaled approximately $2.8 trillion (U.S. GAO) — and the GAO acknowledges this is a substantial undercount because many susceptible programs don’t report at all.

That means the federal government admits to losing roughly $162–$521 billion per year to waste, fraud, and improper payments. The median worker’s $240,000 in lifetime federal income taxes includes their proportional share of this waste: approximately $30,000–$80,000 over a career that went to payments the government itself says should never have been made.

Problem 2: Monopoly Pricing

Government services operate as coercive monopolies — you pay whether you use them or not, and you cannot choose a competing provider. Economic theory and empirical evidence consistently show that monopoly providers charge more and deliver less than competitive alternatives.

The back-of-the-napkin comparison is instructive. The federal government spends approximately $6.75 trillion annually (FY 2024). Of that, roughly $1.0 trillion is pure transfer payments (Social Security, which could be replaced by private retirement accounts), $900 billion is defense (a legitimate debate, but one where $100+ billion in documented Pentagon waste is not controversial), and $800+ billion is Medicare/Medicaid (where the US spends 17.3% of GDP on healthcare versus 10–12% in comparable nations — a gap of roughly $1.5 trillion annually that reflects regulatory capture, not superior outcomes). Private sector administrative overhead runs 5–17% depending on the industry; the federal government’s effective overhead — including compliance costs imposed on citizens and businesses — has been estimated at 20–35% when hidden regulatory burdens are included.

A conservative estimate: if the services currently provided by government were delivered through competitive markets at private-sector efficiency levels, the cost savings would be 30–50% on the service-delivery components — representing roughly $250,000–$400,000 of the median worker’s lifetime tax burden that purchased bureaucratic overhead, waste, and monopoly pricing rather than actual services.

Problem 3: The Seen and the Unseen

The most devastating cost of taxation is not what the government spent badly — it’s what the economy never produced. Every dollar extracted in taxes is a dollar that was not saved, invested, or spent by the person who earned it. The cumulative effect of removing $818,000 from the median worker’s lifetime economic activity — and trillions from the economy as a whole — is reduced capital formation, less entrepreneurship, fewer innovations, and slower productivity growth.

Economists call this the “deadweight loss” of taxation — the economic activity that is destroyed, not merely transferred. Estimates of the deadweight loss range from $0.20 to $0.50 per dollar of tax revenue raised, meaning that for every dollar the government collects, an additional $0.20–$0.50 in economic value is destroyed in the process. Applied to the median worker’s $818,000 lifetime tax burden, this represents an additional $164,000–$409,000 in economic value that simply ceased to exist — jobs not created, businesses not started, innovations not pursued, and compounding growth never realized.

Under a voluntaryist free-market alternative, the services people actually want — roads, dispute resolution, security, education, healthcare, retirement savings — would be provided by competing firms, mutual aid societies, and voluntary associations at market prices, with the discipline of consumer choice replacing the inertia of monopoly. Historical examples are not hypothetical: private roads, private courts (arbitration handles more commercial disputes than government courts today), private schools (which educate at roughly 50–70% of the per-pupil cost of public schools), and fraternal societies that provided healthcare and life insurance to working-class Americans before government programs crowded them out in the mid-20th century.

The $818,000 is not the price of civilization. It is the price of monopoly — and the monopolist has $2.8 trillion in admitted payment errors to show for it.

Summary: The Scale Of The Extraction

The following figures summarize the complete AI model analysis — covering not just fractional reserve banking, but the full architecture of extraction: FRB monetary theft, federal/state/local taxation, and Social Security COLA underpayment through CPI manipulation. All calculations use official BLS 2% CPI as the conservative baseline. Under real inflation (ShadowStats 7–10%/yr), multiply FRB extraction figures by 3–5×.

The Banking System:

• 97% — USD purchasing power lost 1913–2025 (BLS CPI Calculator)

• 1,380× — M2 expansion vs. 100× real GDP growth (Fed H.6)

• $268B — 2024 bank net income, annual (FDIC confirmed)

• $15–25T — Cumulative bank profits 1913–2025 (Modeled estimate)

• $938K — Median worker FRB extraction alone, official CPI (AI Model)

• $1.89M — Median worker delta vs. gold standard (AI Model: Claude/Grok)

The Government:

• $818K — Median worker lifetime tax burden: federal income + payroll + state & local

• ~$190B/yr — Federal savings from CPI manipulation (Four-model consensus)

• $810K — Median retiree SS COLA underpayment over 20-year retirement

The Combined Total:

• $3.52M — Median worker complete extraction: career + retirement (147% of lifetime earnings)

• 42.8 years — Years of the median worker’s 40-year career consumed by the combined extraction

• 116–148% — Percentage of lifetime earnings extracted across all income levels

• 27% — What the median worker actually keeps

• $2.1M–$4.7M — Median worker FRB loss alone under real inflation (ShadowStats/Chapwood) — total extraction under real inflation would be dramatically higher

Every income level from $35K to $1M exceeds 40 years of extraction. The system claims more than a full career from every American worker, then continues extracting through manipulated retirement benefits. These are not independent mechanisms — they are interlocking components of a single extraction architecture in which the banking system creates the inflation, the government taxes the inflated income, and the BLS understates the inflation to reduce the retirement benefits that were promised as compensation for a lifetime of payroll taxes.

The Complete Extraction: Banking System + Government + Social Security Cola Underpayment

When you combine all four mechanisms of wealth extraction — fractional reserve banking, federal taxation, state and local taxation, and Social Security COLA underpayment — a picture emerges that is difficult to dismiss as statistical noise or ideological framing. It is an accounting of where your productive output actually goes.

The median American worker earning $60,000 per year generates $2.4 million in gross lifetime earnings over a 40-year career. Of that amount, the fractional reserve banking system extracts approximately $938,000 through three mechanisms: the inflation tax on wages and savings, the Cantillon Effect that transfers purchasing power to those who receive newly created money first, and the compound trap of interest paid on bank-created money for inflated assets.

Federal, state, and local governments then extract approximately $818,000 through income taxes, payroll taxes, and state and local levies. Under a gold standard with conservative 1% annual productivity deflation — which the US economy actually averaged from 1880 to 1896 during a period of strong real growth — that same worker would have received an additional $951,000 in purchasing power gains that the inflationary system eliminated. The total delta between the current system and an honest monetary system is $1.89 million for the median worker — 32 times their annual income.

But the extraction does not stop when the worker retires.

Over a 20-year retirement, the federal government’s use of understated CPI for Social Security cost-of-living adjustments costs the median retiree an additional $810,000 in benefits they would have received if COLAs reflected actual inflation as measured by ShadowStats or the Chapwood Index rather than the manipulated BLS figures. This is a modeled estimate using the ~7.5 percentage point gap between BLS average COLAs (2.6%/yr) and ShadowStats (10.1%/yr), applied to the median worker’s Social Security benefit of approximately $2,100/month at retirement. This does not include what the worker could have potentially earned if they had been allowed to invest in a potentially more lucrative retirement plan.

The combined total for the median worker: $3.52 million — 147% of gross lifetime earnings. The percentage exceeding 100% reflects the overlapping nature of these mechanisms. The inflation tax erodes your purchasing power while you work; taxes claim a share of your nominal income (which is higher than it would be under stable money); and the SS COLA underpayment continues extracting value during retirement. These are not double-counted — they operate on different streams at different times in your life. The figure exceeding 100% means that the combined extraction is larger than your gross earnings because it includes the retirement-phase theft and the foregone purchasing power gains you would have received under honest money.

Three structural observations from the complete table:

First, the SS COLA column is regressive by design. Because Social Security benefits are capped at the maximum benefit ($3,822/month at full retirement age in 2024), the COLA underpayment flattens at approximately $1.47 million for all earners above $500,000 — but represents 44% of lifetime earnings for the $35K worker versus just 7% for the $500K worker and 0.4% for the $10M earner. The system extracts the most, proportionally, from those who depend on it most.

Second, the banking system and the government are not separate extractors — they are partners in a single mechanism. The banking system creates money that inflates prices; the government taxes your nominal income at rates designed for the inflated price level; the BLS understates the inflation that drives both processes; and Social Security uses that understated inflation to reduce the retirement benefits that were promised as compensation for a lifetime of payroll taxes. Each component reinforces the others. Remove any one, and the system works less efficiently as an extraction mechanism.

Third, the gold standard delta column reveals what was taken from you before you ever earned a dollar. The $720,000 in foregone gold deflation gains for the median worker represents purchasing power that productivity growth would have delivered automatically under honest money — your share of the technological and efficiency improvements your generation produced. Under the current system, those gains are captured by the banking system through inflation and by the government through bracket creep on inflated incomes. You produced the productivity. They captured the gain.

The total across all income levels tells the same story at every scale: the combination of fractional reserve banking, government taxation, and CPI-manipulated benefit underpayment claims between 116% and 148% of what a worker produces over a lifetime of work and retirement. The precise figure varies by income level, but the structural conclusion does not: the system is designed to extract, and it extracts from everyone.

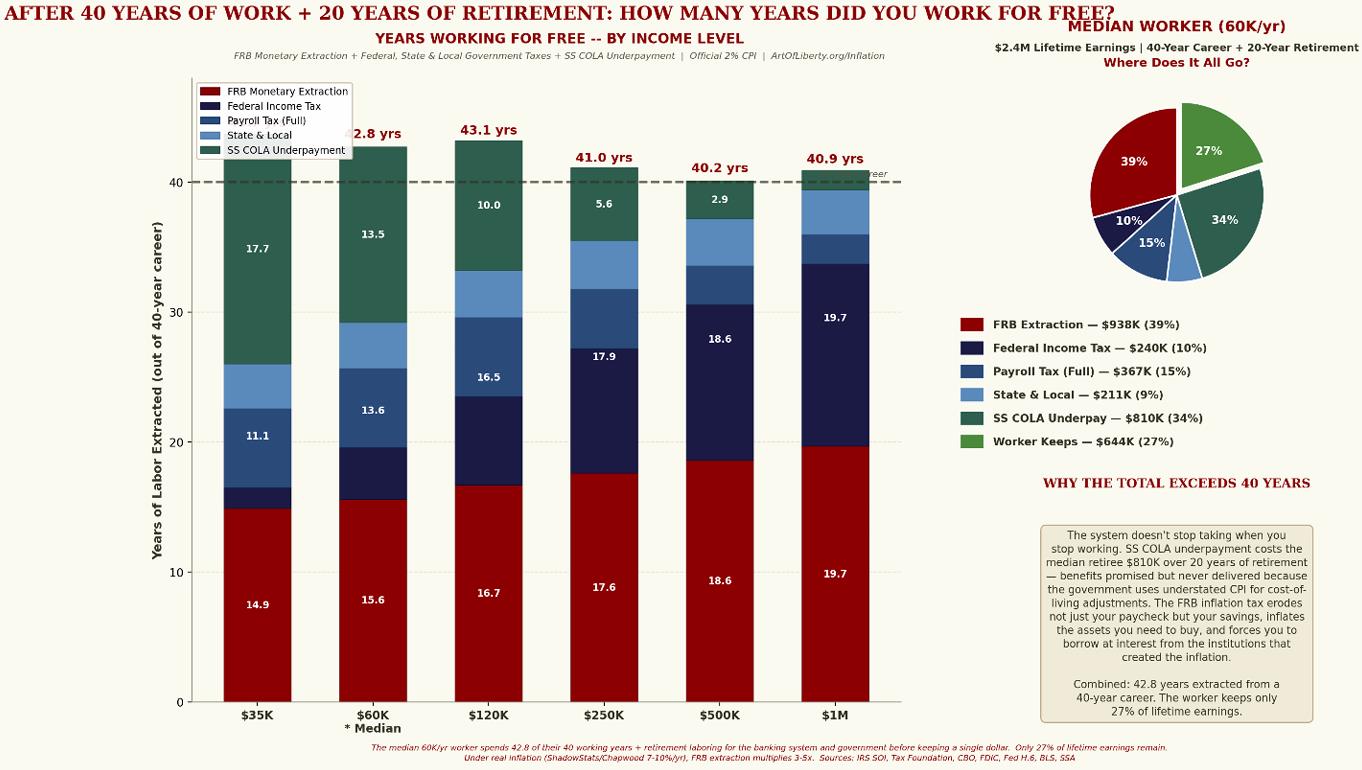

How Many Years Did You (Or Will You) Slave For Free?

Another way to frame the complete extraction: how many years of your 40-year career — plus the 20 years of retirement that followed — were spent working just to cover the wealth transferred to the banking system, the government, and the CPI manipulation that reduces your retirement benefits?

For the median worker at $60K, the combined extraction under official CPI represents 42.8 years of labor — more than the entire 40-year career itself. The worker keeps only 27% of lifetime earnings.

By income level (complete extraction, official CPI):

- $35K earner: 43.7 years.

- $60K earner: 42.8 years.

- $120K earner: 43.1 years.

- $250K earner: 41.0 years.

- $500K earner: 40.2 years.

- $1M earner: 40.9 years.

Every income level exceeds 40 years because the SS COLA underpayment continues extracting value during retirement — the system doesn’t stop taking when you stop working.

The extraction is most devastating for low-income workers: the $35K earner loses 17.7 years to SS COLA underpayment alone (44% of lifetime earnings), while the $1M earner loses only 1.5 years to the same mechanism. The system is regressive by design.

The System Has Many Hallmarks Of An Organized Crime Partnership

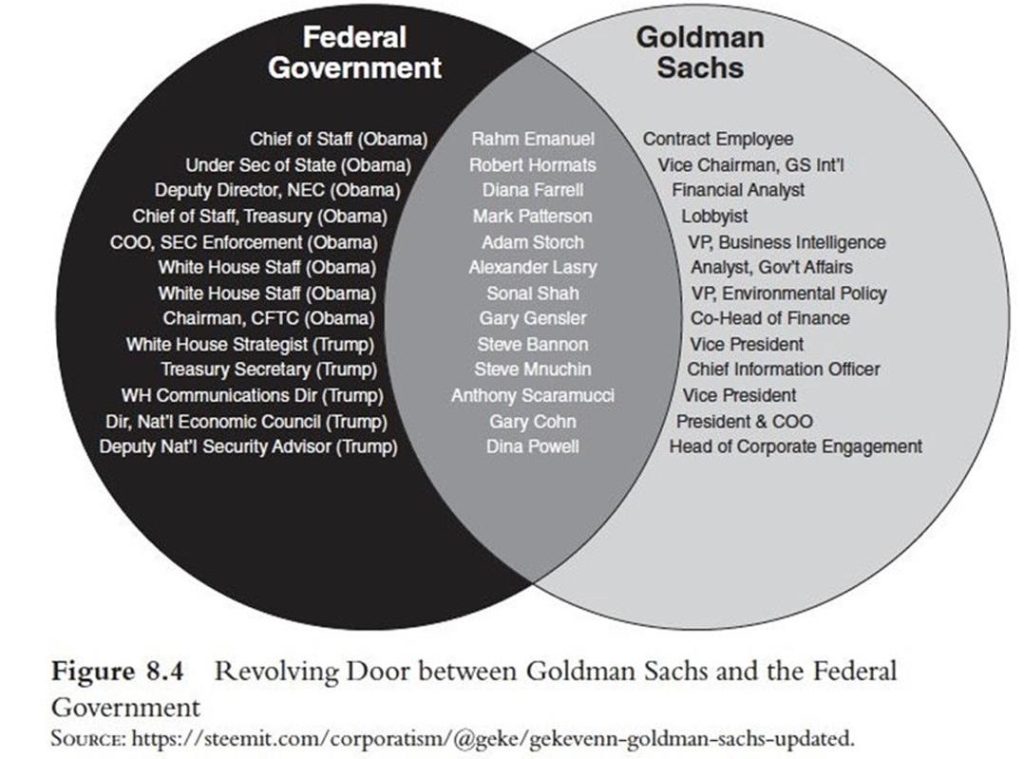

The fractional reserve banking system, as practiced in the United States, exhibits structural parallels to organized criminal enterprise. This is not rhetoric — it is a pattern analysis. Consider the five hallmarks:

Hallmark 1: Regulatory Capture

On January 18, 2019, Cambridge University Press published a study in the Journal of Institutional Economics documenting the revolving door between regulators and the financial industry.

The authors write:

“Looking at the revolving door in the 20 biggest US diversified banks, we identified 304 revolvers, among which 155 are considered as prominent. These revolvers have undertaken 384 revolving door movements between public and private positions and vice versa, mostly between 1960 and 2015, corresponding to a total of 2,256 years of experience in public office.”

This pattern is structural, not incidental. Consider the architecture of the capture:

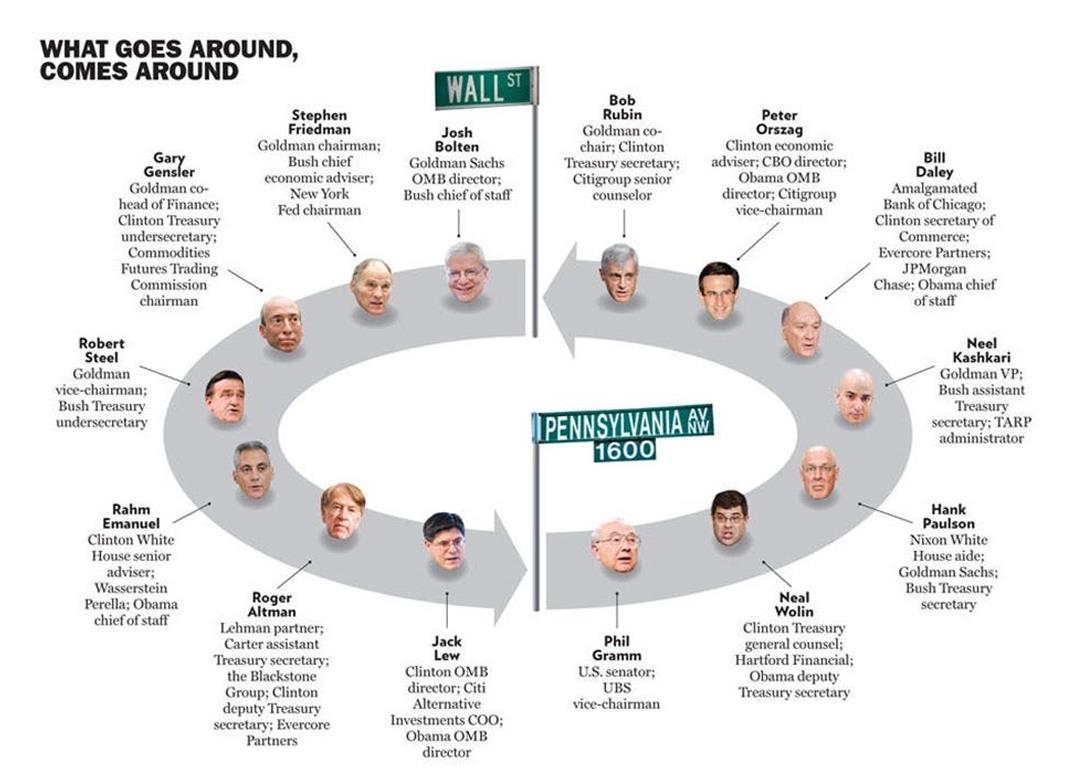

• Timothy Geithner went from President of the NY Federal Reserve Bank directly to Treasury Secretary, then to Warburg Pincus private equity.

• Robert Rubin spent 26 years at Goldman Sachs, became Treasury Secretary under Clinton — where he repealed Glass-Steagall separating commercial and investment banking — then joined Citigroup’s board, which immediately benefited from the deregulation he championed.

• Hank Paulson was CEO of Goldman Sachs before becoming Treasury Secretary and administering the 2008 bailout that saved Goldman from its own bad bets.

These are not anomalies; they are the system operating as designed. The revolving door is not corruption of the regulatory process — it is the regulatory process.

Hallmark 2: Capture Of The Economics Profession

2012 AIER Article: American Economic Association: Only 487 economists list “monetary policy, central banking, and the supply of money and credit,” as either their primary or secondary specialty; 310 list “money and interest rates.”

Federal Reserve’s Board of Governors employs 220 PhD economists. The 12 regional banks employ scores more. The Fed also doles out millions of dollars in contracts to economists for consulting assignments, papers, presentations, workshops, and that plum gig known as a “visiting scholarship.”

A Fed spokeswoman says that exact figures for the number of economists contracted with weren’t available. But, she says, the Federal Reserve spent $389.2 million in 2008 on “monetary and economic policy,” money spent on analysis, research, data gathering, and studies on market structure; $433 million was budgeted for 2009. 84 of 190 editorial board members across top journals had Fed ties.

The implications are profound: when virtually every prominent macroeconomist has either worked for the Federal Reserve, received Fed research grants, or depends on Fed data access for publication, the field cannot produce independent criticism of central banking.

This dynamic was documented starkly in the 2010 documentary “Inside Job,” in which Columbia economist Frederic Mishkin — a former Fed governor — was shown to have been paid $124,000 by the Icelandic Chamber of Commerce to write a paper praising Iceland’s financial system shortly before its collapse. Mishkin had listed the paper on his CV as “Financial Stability in Iceland” but changed the title to “Financial Instability in Iceland” after the crash.

The economics profession’s dependency on central bank funding is the primary reason mainstream economics has never seriously challenged the legitimacy of money creation ex nihilo. Academics who depend on Fed grants do not publish research quantifying the cost of the Fed’s money-creation system to ordinary workers. This is not conspiracy theory — it is institutional incentive structure.

Hallmark 3: Capture Of The Federal Government

The Federal Reserve system was designed by bankers, for bankers, and delivered to bankers by a compliant Congress. The 1913 Federal Reserve Act was drafted at a secret meeting at Jekyll Island, Georgia, attended by representatives of J.P. Morgan, the Rockefeller interests, and the National City Bank of New York. The resulting institution grants private banks the exclusive privilege of creating money through lending — a privilege enforced by the federal government and backstopped by taxpayer-funded deposit insurance.

Campaign Contributions And Lobbying: The Financial Sector’s Political Investment

The Finance, Insurance, and Real Estate (FIRE) sector is the largest source of campaign contributions to federal candidates and parties in the United States — and has held that position for decades. This is not a contested claim. It is documented by OpenSecrets (formerly the Center for Responsive Politics), the nonpartisan organization that compiles Federal Election Commission data into searchable public records.

Scale of Contributions

According to OpenSecrets’ aggregated FEC data, the FIRE sector has been either the largest or second-largest contributing industry group in nearly every federal election cycle since tracking began in 1990.

Cumulatively from 1990 through 2024, total contributions from the financial sector exceed $20 billion in nominal terms, with substantial portions directed toward members of key committees overseeing banking, taxation, and financial regulation.

The securities and investment sub-industry alone was responsible for nearly $805 million in contributions during the 2020 cycle, with the majority flowing through soft money and outside spending groups. In the 2022 cycle, total FIRE sector political spending exceeded $3.5 billion. In the 2024 cycle, the sector again ranked as the top contributor to PACs, political parties, and candidates, with securities and investment firms leading all industries.

The sector’s PAC contributions to federal candidates in the 2024 cycle totaled $82.6 million, of which commercial bank PACs contributed $11.6 million. But PAC contributions represent only a fraction of total influence spending. When individual contributions over $200, party committee donations, soft money, and outside spending groups are included, the per-cycle total routinely exceeds $1 billion in direct political contributions alone.

Lobbying: The Larger Channel

Campaign contributions are the visible portion of the financial sector’s political investment. The larger channel is lobbying. Federal lobbying spending reached a record $4.4 billion across all sectors in 2024. The FIRE sector spent $636.4 million on lobbying that year — an increase of $33.8 million over the prior year — making it the second-largest lobbying sector after health care.

No other sector has historically spent as much on lobbying as the financial industry. Since 2007, the top three lobbying sub-sectors within FIRE have consistently been insurance, securities and investment, and real estate. Total lobbying expenditures across all sectors have increased by more than $1 billion over the past decade, totaling nearly $37 billion since 2015.

The Combined Investment

When campaign contributions and lobbying are combined, the financial sector spends roughly $1.5–$2.0 billion per two-year election cycle to influence federal policy. This figure does not include dark money organizations, 527 political nonprofits, state-level contributions, or the revolving door appointments documented elsewhere in this report — all of which represent additional channels of influence that are harder to quantify but no less consequential.

The Return on Political Investment

The return on this investment is extraordinary by any measure. The financial sector spends approximately $1.5 billion per cycle on political influence and receives, in return, the exclusive privilege of creating money through fractional reserve lending — a privilege enforced by the federal government and backstopped by taxpayer-funded deposit insurance. That privilege generated $268 billion in audited net income in 2024 alone (FDIC Quarterly Banking Profile). On a per-cycle basis, that represents a return of roughly 180:1 on political investment — before counting the approximately $190 billion per year the government saves through CPI manipulation that benefits both the banking system (by understating the inflation their money creation produces) and the government (by reducing indexed obligations to retirees and veterans).

Over the full period from 1990 to 2024, the sector has spent approximately $20 billion on political contributions and an estimated $15+ billion on lobbying — roughly $35 billion combined. During that same period, the banking system earned an estimated $7–$10 trillion in cumulative net income. The political investment represents approximately 0.3–0.5% of the profits it protects.

Interpretation

These contributions do not prove direct control over specific policy outcomes — and making that claim is unnecessary. What they demonstrate is a structural environment in which the financial sector maintains persistent, large-scale engagement with the political system; preferential access to lawmakers and regulators through both contributions and the revolving door; and a policy feedback loop in which the institutions that benefit most from the current monetary architecture are also the largest funders of the political system that maintains it.

When viewed alongside the regulatory capture documented earlier in this report (304 revolving-door hires, 2,256 cumulative years of public office across the 20 largest banks), the economics profession’s dependency on Federal Reserve funding, and the media’s reliance on financial-sector advertising revenue, campaign finance represents the third major channel of institutional influence — and the one with the most complete public documentation.

Hallmark 4: Capture Of Academia

Compulsory government schooling systems in the United States teach children that “government” is legitimate, desirable and necessary before they are old enough to evaluate the morality and logic of that claim. The mandatory government schools and accredited private schools never evaluate the illogic and immorality of “government” on its face: the inability for the population to have delegated the government “rights” (taxation/theft, ability to make up rules, etc.) that they do not possess themselves, the inability to be bound to a social contract they did not sign, and democracy’s moral equivalency to lynching and gang rape.

The Federal Reserve is presented as a neutral public institution that “stabilizes the economy,” that inflation is a natural and manageable phenomenon, and that banking is a productive profession that allocates capital efficiently.

What they do not teach:

-

That the Fed is a private institution owned by member banks

-

That its “price stability” mandate explicitly targets 2% annual currency destruction

-

That fractional reserve banking was criminalized in many early American colonies

-

That three serious attempts to establish a central bank were defeated by presidents who understood the mechanism

Andrew Jackson — who killed the Second Bank of the United States in 1832 — called central bankers “a den of vipers and thieves” and is arguably the last president to have directly confronted the banking cartel and won. That lesson does not appear in any government school curriculum.

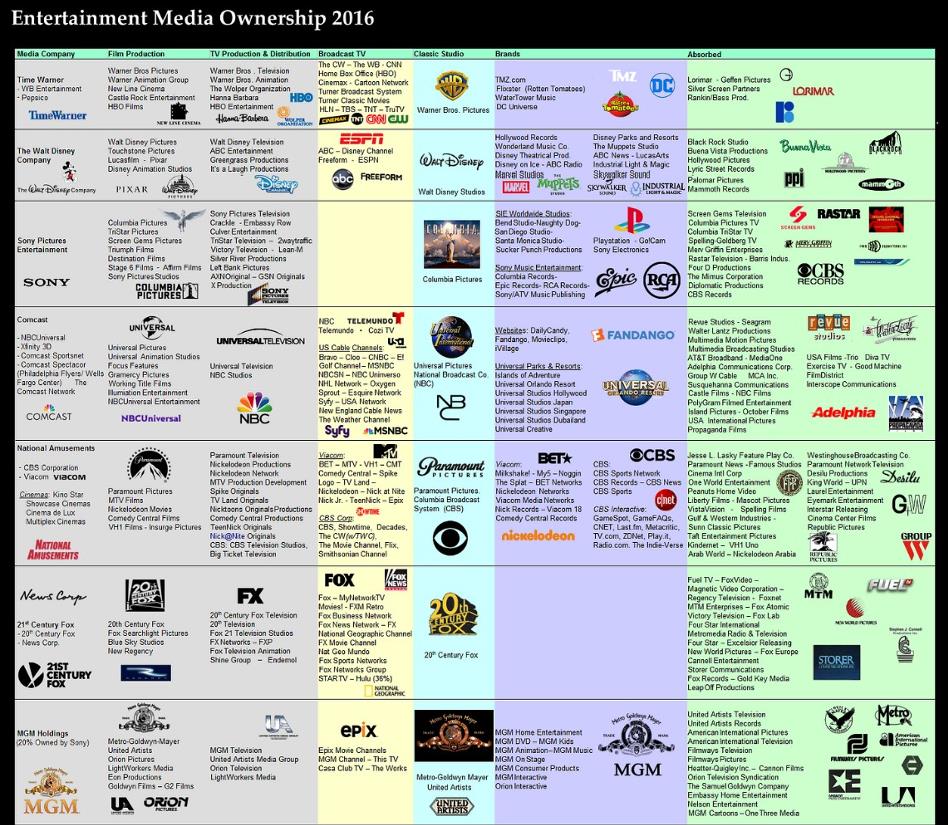

Hallmark 5: Monopolization Of The Media And The Internet

In 1983, approximately 50 corporations controlled the majority of American media. By 2023, six corporations — Comcast, Disney, Warner Bros. Discovery, Paramount, News Corp, and Sony — control approximately 90% of what Americans see, hear, and read. The consolidation was financed with cheap debt from the very banking system being normalized.

Media companies depend on financial-sector advertising revenue and are increasingly owned by the same institutional investors who benefit from the system. The result is a media ecosystem structurally incapable of challenging its own financiers: no major network has produced a serious investigative piece on fractional reserve banking as a mechanism of wealth transfer. The mechanism is not primarily censorship — it is ownership. You do not need to suppress stories when the people who would publish them work for the people who benefit from them not being published. The result is a near-complete information blackout on the single largest wealth transfer in American history.

The internet initially threatened this control, which is why — beginning around 2016 — algorithmic demotion of heterodox economic content, demonetization of channels discussing central banking critically, and outright platform bans for monetary dissidents became standard practice across YouTube, Facebook, and Twitter/X.

On October 11, 2018, Facebook and Twitter executed a coordinated purge of over 800 pages and accounts, including The Free Thought Project (3.1 million followers), Anti-Media (2.1 million followers), Cop Block, Police the Police, and the personal accounts of journalists like Rachel Blevins. Facebook claimed the pages violated rules against “spam” and “coordinated inauthentic behavior,” but the targeted outlets were verified pages that had spent years building audiences around government accountability, police brutality documentation, and anti-war journalism. The purge was later linked to Facebook’s partnership with the Atlantic Council’s Digital Forensic Research Lab — a NATO-affiliated think tank funded by Gulf monarchies, defense contractors including Raytheon and Lockheed Martin, and the US government.[11]

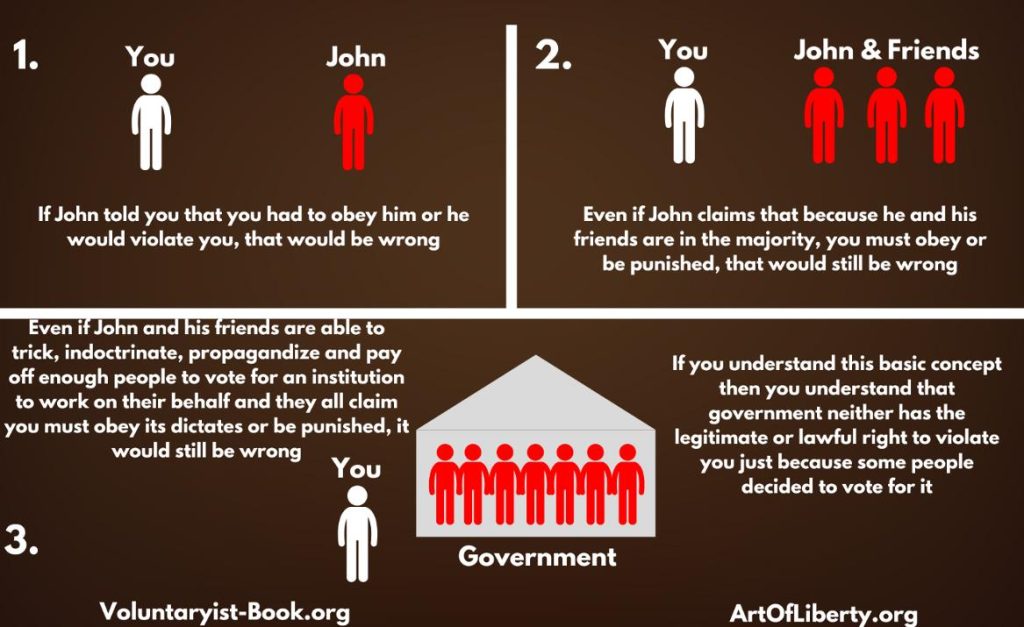

The Voluntaryist Case: The Ethical Foundation

The analysis in this report is economic. But the conclusion is ethical. No legislative process can make theft legitimate. The fractional reserve banking system transfers wealth from those who earn it to those who create the medium of exchange — without the informed consent of the people whose purchasing power is diluted. This is not a bug in the system. It is the system and it is inherently criminal.

Voluntaryism, also known as the Philosophy of Human Respect, holds that all human interaction should be voluntary. This philosophy is grounded in three axioms of human nature: every person has a fundamental drive to be happy; physical harm always decreases a person’s happiness; and theft or property damage always decreases the owner’s happiness. These are not opinions — they are observable features of human experience. A system built on inflation, taxation, and monetary dilution violates all three simultaneously, and does so by design.

No one can use violence or force on anyone else, except defensively, and no one has an exception from morality — especially the “government.” Since “government” relies on extortion and force it is obviously illegitimate, immoral and illogical.

We believe it was either:

-

The dumbest idea in history — Creating a ruling class with a monopoly on violence and rulemaking and expecting that it could be disciplined by a piece of paper.

-

A scam from the beginning — An illegitimate, immoral, illogical and easily rigged system that the population was tricked into by the “Brute Force Manufactured Consensus” of the banker’s media dominance of the time and ongoing mandatory indoctrination and unethically manipulative propaganda in the modern era.

Either way, since it is impossible to have a moral and legitimate “government,” we have to extract ourselves from what is obviously a criminal enterprise in Washington, DC.

The Federal Reserve system is either a creature of the “government” (or the “government” is a creature of the Federal Reserve). The Fed is backed by government force and violates freedom of choice at every level: compulsory legal tender laws force acceptance of depreciating currency; compulsory taxation funds the regulatory apparatus that protects the banks; and compulsory education ensures the mechanism is never exposed.

The alternative is not chaos. It is consent. Let people choose their money, choose their banks, and choose whether to participate in a system that costs the median worker $938,000–$4.7 million over a lifetime. Given the choice, no rational person would consent. That is why the choice has never been offered.

Right now, we are in an information war with the bankers and “government” where organized crime has bought up and monopolized the media to trick the population into thinking the system is legitimate.

What The Market Would Have Done

In the absence of fractional reserve banking and central bank intervention, the free market would have produced four outcomes that the current system actively suppresses:

-

Productivity-driven deflation: As technology improves and efficiency rises, prices should fall. Under a stable money supply, the same dollar buys more over time. Workers get richer automatically, without raises. This is the natural state the banking system stole.

-

Stable purchasing power: Without money creation beyond productivity growth, the dollar would hold its value. The 97% loss since 1913 would not have occurred.

-

Market-rate interest: Without Fed rate manipulation, interest rates would reflect actual savings and time preference, not political expediency. Bubbles and crashes would be smaller and self-correcting.

-

No gold confiscation: Executive Order 6102 (April 5, 1933) forced Americans to surrender their gold at $20.67/oz. The government then immediately revalued gold to $35/oz — a 69% overnight devaluation of every American’s savings. This was theft by executive decree, made necessary only because the fractional reserve system had expanded the money supply beyond what gold reserves could support.

Full Reserve Banking: Protection For Workers Who Want It

Full reserve banking — where banks must hold 100% of depositors’ funds and can only lend from time-deposit accounts where the depositor has explicitly agreed to lock up their money — is not a radical proposal. It was advocated by Irving Fisher, Milton Friedman, and the “Chicago Plan” economists in the 1930s. A 2012 IMF Working Paper (Benes & Kumhof, “The Chicago Plan Revisited”) modeled full reserve banking and found it would reduce economic volatility, eliminate bank runs, and dramatically reduce public and private debt.

The free-market alternative is simple: let people choose. Those who want the potential returns of fractional reserve banking can accept the risk. Those who want safe storage of their purchasing power should have the option of full-reserve accounts. Currently, the system forces everyone into fractional reserve banking whether they understand it or not — and taxpayers guarantee the downside through FDIC insurance.

What You Can Do

-

Educate Yourself: Read the full analysis at artofliberty.substack.com. Understand the three mechanisms. Know the numbers for your income level.

-

Share This Report: This document is Creative Commons. Print it, email it, post it. The system survives on ignorance; every person who reads this becomes harder to extract from. You can buy printed copies from ArtOfLiberty.org/Store.

-

Test It Yourself: Open any AI model and replicate the analysis. The prompts are in this report. When you see the numbers from your own independent verification, the reality becomes undeniable.

-

Move Your Money: Research credit unions, full-reserve banking options, sound money, and decentralized alternatives. Every dollar you remove from the fractional reserve system is a dollar that can’t be leveraged 10:1 against you. Use Cash! Cash saves your local merchants 1.5–3.5% while simultaneously starving the banks of 1.5–3.5%. It allows merchants to under-report their income, starving the organized crime “government” and keeping more cash in the community, which has a variety of benefits.

-

Demand Transparency: Ask your elected representatives why the cost of fractional reserve banking to ordinary workers has never been officially calculated. Ask why the BLS uses methodology that understates inflation. Ask why 12 years of public education never mentions how money is created. This is the study that should have been done 100+ years ago if the “government” was really about protecting life, liberty, and property. The fact that it has never been done until now by a private foundation is proof-positive that the “government” has been a willing accomplice to this theft.

-

Embrace Voluntaryism: The system persists because it has been declared “legal” by the same government it captured. No one can ethically force you into a monetary system that steals from you. Voluntary exchange, honest money, and consent-based institutions are the alternatives. Visit ArtOfLiberty.org and Voluntaryism-Book.org.

-

Support Our Work: Become a sponsor of the Art of Liberty Foundation at ArtOfLiberty.org/Sponsor. We have some amazing perks to say THANK YOU! and help your friends, family, and colleagues understand the scam of “government” and the rapidly depreciating fiat paper tickets and digital dollars issued by organized crime banks.

About The Authors

Etienne de la Boetie² is the founder of the Art of Liberty Foundation and an internationally recognized expert and speaker on voluntaryism and government illegitimacy, criminality, and corruption. He is the author of “Government” – The Biggest Scam in History… Exposed! – How Inter-Generational Organized Crime Runs the “Government,”Media and Academia and To See the Cage Is to Leave It – 25 Techniques the Few Use to Control the Many, and the editor of the Art of Liberty Daily News and Five Meme Friday, which delivers hard-hitting voluntaryist memes and the best of the alternative media. His original writing and research can be found at ArtOfLiberty.Foundation and, in Spanish, at ArteDeLaLibertad.org.

About The Ai Co-Authors

This analysis was conducted with four independent AI models: Anthropic’s Claude (Sonnet), xAI’s Grok, Google’s Gemini, and OpenAI’s GPT. Each was prompted independently with identical data and methodology parameters. Their convergent results strengthen the findings by demonstrating that the extraction pattern is visible to any sufficiently capable analytical system, regardless of corporate ownership or training bias.

Connect With The Art Of Liberty Foundation

ArtOfLiberty.org — Main Foundation website. Research, reports, and resources.

ArtOfLiberty.Foundation — Etienne’s writing and our Investigative Reports and Journalism.

VoluntaryistNews.org — Art of Liberty Daily News – The best of the alternative news curated from a voluntaryist perspective.

FiveMemeFri.org — Hard-hitting voluntaryist memes and the best of the alternative media.

Government-Scam.com — The companion book: “Government” — The Biggest Scam in History… Exposed! – How Inter-Generational Organized Crime runs the “Government,” Media and Academia.

SeeTheCage.com — Etienne’s new book: To See the Cage is to Leave It – 25 Techniques the Few Use to Control the Many.

Voluntaryism-Book.org — Voluntaryism — How the Only “ISM” Fair for Everyone Leads to Harmony, Prosperity and Good Karma for All. Upcoming! Read sample chapters and get notified.

ArteDeLaLibertad.org — The Art of Liberty Foundation in Español!

A Note On Methodology And Intellectual Honesty

This report makes extraordinary claims. Extraordinary claims require transparent methodology. Every figure in this analysis falls into one of three categories:

Confirmed (hard data): FDIC-reported bank net income ($268B, 2024). Fed H.6 money supply data ($21.5T M2). BLS CPI calculations (97% purchasing power loss since 1913). These are audited, published, and independently verifiable.

Calculated (derived from hard data): Lifetime extraction by income level. These use confirmed inputs (CPI rate, wage data, mortgage rates) in a standard economic framework. The calculations can be replicated by anyone with a spreadsheet or an AI model.

Modeled estimates: Cumulative bank profits ($15–25T). Gold standard counterfactual gains. These require assumptions about historical profitability and alternative monetary regimes. We label them clearly and explain the assumptions.

Where critics can legitimately challenge this analysis: the Cantillon Effect magnitude (we use a conservative 3% annual divergence — others argue higher); the gold standard counterfactual (no one can know with certainty what would have happened); and the ShadowStats/Chapwood multiplier (real inflation is genuinely difficult to measure, which is itself part of the problem).

Where critics cannot legitimately challenge this analysis: that fractional reserve banks create money through lending (Bank of England, 2014); that money creation is inflationary (monetary economics 101); that inflation transfers purchasing power from later recipients to earlier recipients (the Cantillon Effect, 1755); and that the median American worker’s purchasing power has stagnated while financial sector profits have grown exponentially (FDIC, Fed, BLS).

The Four Metrics: Detailed Methodology

Metric 1 — Total Bank Net Income (1913–2025): Based on FDIC Quarterly Banking Profile data for insured commercial banks, extrapolated backward to 1913 using historical banking industry profitability rates and inflation-adjusted to 2025 dollars. Range: $15–25 trillion (modeled estimate). The 2024 confirmed figure of $268 billion annual net income anchors the modern end.

Metric 2 — Cost to Median Worker (Lifetime): Three-mechanism calculation: inflation tax (purchasing power erosion on wages and savings), Cantillon Effect (asset-price divergence from wage growth), and compound trap (interest on bank-created money). 40-year career, official 2% CPI baseline. Result: $938K (official CPI) to $4.7M (real inflation).

Metric 3 — M2 Money Supply Expansion: Fed H.6 data: M2 grew from approximately $25 billion (1913) to $21.5 trillion (2025) = 1,380× expansion. Real GDP grew approximately 100× over the same period. The excess ~14× represents pure monetary dilution — purchasing power transferred from holders of existing money to creators of new money. 1,380×

Metric 4 — Annual Debtor Burden: Approximately $780 billion in annual interest payments on bank-created money across mortgages, student loans, auto loans, and consumer credit. This is the compound trap expressed as a flow rather than a stock. Note: this figure represents total debtor costs, not bank profit — bank net income of $268B is a subset.

Glossary Of Key Terms